+44-7511-112566

+44-7511-112566 +353-1-8079571

+353-1-8079571 +1-415-799-9792

+1-415-799-9792

Top 20 Blockchain Project Ideas for 2022

Also referred to as the Distributed Ledger Technology or DLT, blockchain technology is one of the emerging

Also referred to as the Distributed Ledger Technology or DLT, blockchain technology is one of the emerging

The global Blockchain market is projected to stand at 39 bn USD by 2025 as the

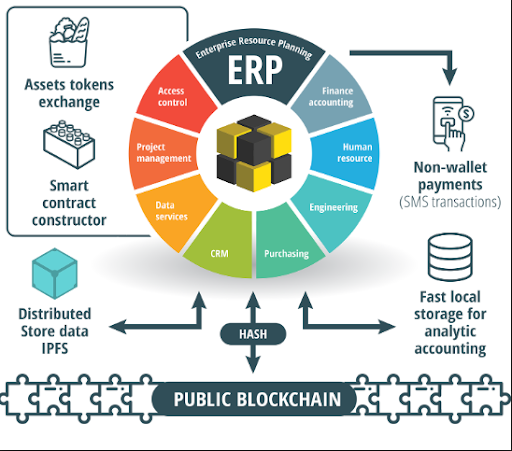

Blockchain can influence our daily life, it becomes important that it is able to connect to various business application

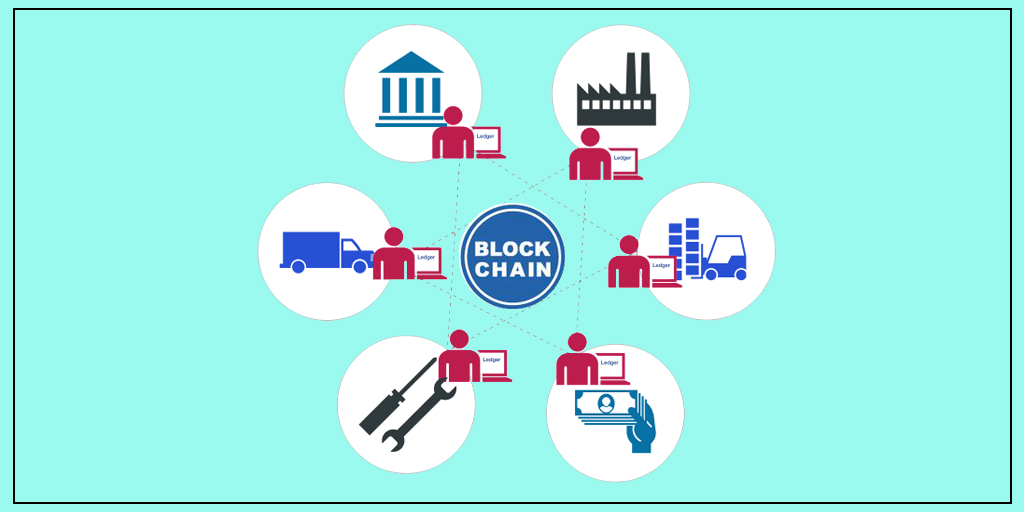

A blockchain is a decentralized, distributed record or “ledger” of transactions in which the

Cryptocurrency\’s fever is spreading like wildfire. Out of the total wealth out there (approximately $84 trillion).